Wondering about plan changes to the bridge benefit? - Public Service

Wondering about plan changes to the bridge benefit?

Find out how changes to the bridge benefit and lifetime pension may help improve your years of retirement.

If there is one constant in life, it's that things change over time. Today, it costs more to buy a house and go to school, and the price of a bag of groceries can sometimes be a shock. Life expectancy and employment patterns, too, have changed – we're living longer and working later – and this is reflected in recent plan changes to the bridge benefit and lifetime pension.

Why the bridge benefit changed

Early retirement features were designed almost 50 years ago. The bridge benefit was intended to be a short-term, temporary benefit that would bridge the gap between early retirement and age 65, when government benefits traditionally began.

But times have changed. British Columbians, including many plan members, are

- changing jobs more often,

- starting jobs with plan employers later in their careers, or

- working longer due to personal choices or circumstances.

Only members who could retire before age 65 could take advantage of the bridge benefit. So while all members paid for the bridge benefit, only a certain portion of members could take it. This was not fair for all members.

How the plan is now more equitable

For regular members

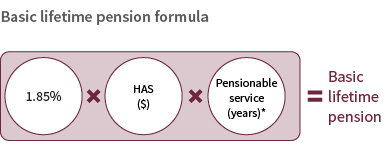

To better reflect the current working environment and make the plan more equitable, effective April 1, 2018, the lifetime pension accrual rate increased to a flat rate of 1.85 per cent and the bridge benefit was removed for service earned from April 1, 2018, onward.

Changes effective April 1, 2018

- Lifetime pension accrual rate increased to 1.85 per cent

- Bridge benefit removed

The bridge benefit has not disappeared entirely, however. It still applies for service earned before April 1, 2018. In addition, the lifetime pension and bridge benefit rates for service earned between April 1, 2006 and March 31, 2018, have been adjusted to improve service for this period.

For ambulance paramedics

Effective April 1, 2020, the lifetime pension accrual rate increased to a flat rate of 1.85 per cent and the bridge benefit was removed for service earned from April 1, 2020, onward.

Changes effective April 1, 2020

- Lifetime pension accrual rate increased to 1.85 per cent

- Bridge benefit removed

The bridge benefit has not disappeared entirely, however. It still applies for service earned before April 1, 2020. In addition, the lifetime pension and bridge benefit rates for service earned between April 1, 2006 and March 31, 2018, have been adjusted to improve service for this period.

Note for correctional members

Correctional members still accrue a bridge benefit. For more information on the plan design changes for correctional members, please see the Plan Changes section of the website.

What these changes mean for affected members

These changes are good news for regular members and ambulance paramedics. The rate increase will boost your long-term savings because the lifetime pension accrual rate is one of the things used to calculate your pension benefit, along with salary and years of service.

HAS = highest average salary: the average amount of your salary during each of the highest five years of salary

* To a maximum of 35 years

How your past service is improved

If you earned service between April 1, 2006 and March 31, 2018, inclusive, your lifetime pension accrual rate has increased from 1.35 to 1.65 per cent and the bridge benefit accrual rate correspondingly decreased from 0.65 to 0.35 per cent for your salary below the year's maximum pensionable earnings (YMPE) during that period. This means your pension up to age 65 remains the same, and your lifetime pension after 65 will increase.

Changes effective October 1, 2019, for salary below YMPE

- Lifetime pension accrual rate increased to 1.65 per cent

- Bridge benefit accrual rate decreased to 0.35 per cent

Changes effective October 1, 2019, do apply to correctional employees and BC Ambulance Service paramedics.

How these changes all work together

Here's an example of how it all works. Let's say you are a regular member and retire at age 57 on March 31, 2019, after spending 28 years working full time and contributing to the plan.

You earned 15 years of service before April 1, 2006; 12 years between April 1, 2006 and March 31, 2018; and 1 year as of April 1, 2018.

Your total pension is calculated using three different accrual rates:

- Before April 1, 2006 – 15 years of service at 1.35 per cent lifetime pension and 0.65 per cent bridge benefit

- Between April 1, 2006 and March 31, 2018 – 12 years of service at 1.65 per cent lifetime pension and 0.35 per cent bridge benefit

- From April 1, 2018 – 1 year of service at 1.85 per cent lifetime pension and no bridge benefit

Since you’re retiring eight years before the normal retirement age of 65, the bridge benefit amount you'll receive up to age 65 reflects the percentage of your service earned in each of the three periods – in this example, only one year falls under the new rules (April 1, 2018, onward) where there is no bridge benefit.

Note: if you retire early and your pension is reduced, any bridge benefit that applies to your service will also be reduced; this calculation will be incorporated into the estimate you receive on your annual member benefit statement or in My Account.

Your plan is fair and forward-thinking

Remember, the plan is designed to provide financial stability in retirement that is fair for all members; recent plan changes also help improve lifetime pensions for members overall. In a shifting world, it makes sense to plan for the long term, and your pension plan can help you face the future with assurance.

For more details, see Plan changes.

Related content for Wondering about plan changes to the bridge benefit?

What is the year's maximum pensionable earnings?