How sturdy is your retirement income? - Public Service

How sturdy is your retirement income?

Learn about the sources of income that can help you build a solid financial plan for retirement.

Your pension

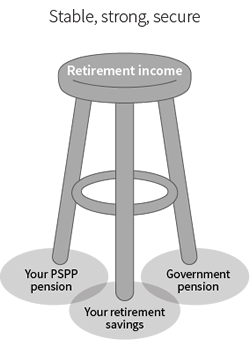

Some financial planners talk about retirement income as a three-legged stool – with the three legs being your workplace pension, personal savings and government pension programs. The idea is that you need all three to provide a stable source of income in your retirement.

In the three-legged stool scenario, you can count on the solid support of your pension from BC's Public Service Pension Plan. Your pension will provide you with a dependable and regular source of income for your lifetime.

In the three-legged stool scenario, you can count on the solid support of your pension from BC's Public Service Pension Plan. Your pension will provide you with a dependable and regular source of income for your lifetime.

But how much income will it actually provide? Use the personalized pension estimator to get a good sense of your potential annual pension income.

What happens if you retire early? Can you buy back service for a leave of absence to increase your pension? How do different pension options affect your potential monthly pension payments? Your Member’s benefit statement is also a good source of information.

Government pensions

Your pension from the Public Service Pension Plan may not be your only source of retirement income. Government pensions such as the Canada Pension Plan (CPP) and old age security (OAS) are other sources of income after you stop working.

CPP pays you a monthly income when you retire. The amount you receive is based on how long you’ve contributed to CPP and the amount of your contributions. You can apply as early as age 60, although your payments will be lower than if you apply at a later age.

You may also be eligible for an OAS pension as early as age 65, if you meet citizenship and residency requirements.

You have to apply directly for these government pensions when you are ready to receive them.

A useful tool for estimating your retirement income is the federal government’s Canadian Retirement Income Calculator. This online tool can help you estimate your retirement income from both your workplace and government pension sources.

Once you have a sense of your potential annual retirement income from the Public Service Pension Plan and government pensions, you’ll be in a better position to know if there’s a shortfall between what you will need and what you will have.

Personal savings

Personal savings is the final leg of the three-legged stool. Tax-free savings accounts and RRSPs are often used to save money for long-term goals such as retirement.

Many people wonder if you can contribute to an RRSP when you are a member of a pension plan. The answer is yes. However, the amount you are allowed to contribute to an RRSP will be lower because you are already contributing to a registered pension plan.

Knowledge is power

Planning for your retirement is time well spent. Just a few minutes with the personalized pension estimator and a half hour on the federal government’s retirement income calculator is a great way to see if you are on track for the retirement income you’ll need.

It's also a good idea to talk with an independent financial adviser about how your pension fits in your retirement plan and how it can provide an important source of income for those you love.

Remember, your pension from the Public Service Pension Plan is just one of the three legs on the stool of retirement income. You also need to think about the other two supports: government pension programs and your personal savings. You want to make sure these two legs are in place, and that they are sturdy enough to provide you with the support you need when you retire.

Remember, your pension from the Public Service Pension Plan is just one of the three legs on the stool of retirement income. You also need to think about the other two supports: government pension programs and your personal savings. You want to make sure these two legs are in place, and that they are sturdy enough to provide you with the support you need when you retire.

External links for how sturdy is your retirement income

Canadian Retirement Income Calculator

Apply for the Canada Pension Plan